The second quarter of 2024 saw copper prices surge on the London Metals Exchange (LME) on the back of supply bottlenecks and elevated demand, particularly from energy sectors.

Copper markets saw momentum from the first quarter with prices on April 3 sitting at US$8,728 per metric ton, but supply and demand dynamics provided critical support for the base metal and by the end of the month, the price had climbed to US$9,973.50.

With an improving macroeconomic environment in the United States increasing the likelihood of a rate cut and continued cuts at Chinese refiners in May, the copper price encountered a perfect storm that helped the metal set a record high on the LME of US$11,104.50 per metric ton on May 20, and it hit an even higher price on the COMEX of US$5.20 per pound, or US$11,464 per metric ton, the same day.

The copper price pulled back to end Q2 at US$9,418 per metric ton. Although the price has since retreated to US$9,051.50 as of July 22, it remains at elevated levels with conditions likely to continue providing support for the near future.

Copper price chart, January 1 to June 30, 2024.

Chart via London Metal Exchange.

Copper supply struggles lead to tight market in Q2

Both the loss of existing copper supply and the lack of incoming supply are supporting copper prices this year.

Weighing on copper supply has been the closure of First Quantum’s (TSX:FM,OTC Pink:FQVLF) Cobre Panama mine in Panama, which accounted for approximately 1 percent of global copper supply when it was operational.

The mine is currently in care and maintenance with negotiations halted as First Quantum awaited the results of presidential elections this past May. The newly elected José Raúl Mulino, a conservative, was seen as an investor favorite. However, Mulino has said his government won’t engage in a fresh round of negotiations unless First Quantum drops its arbitration claims.

“From what I understand most of the people that were running for presidential election were all against the project,” Mazumdar said. “I don’t think there’s anybody there that is for the project winning. So then it’s all about arbitration, which will drag on for a while.”

He believes the situation will impact investment decisions elsewhere as well. “It will also make people and companies rethink spending a lot of money in some jurisdictions if they don’t have government support.”

Elsewhere in the sector, the news has been mixed at best. Despite predicting lower grades and reduced production at its Quellaveco mine, Anglo American (LSE:AAL,OTCQX:AAUKF) saw an 11 percent year-over-year increase during the first quarter as the mine achieved its highest throughput rate. Even so, the copper miner has set guidance for copper production at 730,000 to 790,000 metric tons for 2024, substantially lower than the 826,000 metric tons of copper production it saw in 2023.

“We’ve also had a secular negative trend in production with the largest copper producer, which is Codelco. They’ve got problems with large amounts of debt, so their ability to fund their expansions is problematic,” Mazumdar said.

Codelco, Chile’s state-run mining company, saw production slump to 25 year lows in 2023. This year, the world’s largest copper producer is struggling to meet its 2024 production targets as a new mandate from the Chilean government has prioritized lithium production and the Chuquicamata and El Teniente mines continue to be plagued by long-term debt issues.

Lower production levels have stressed treatment charges since the start of the year, forcing Chinese refiners to begin their own production cuts earlier in the year. However, these cuts have done little to raise margins and producers have begun to plan for additional cuts in Q3 as lowered rates begin to affect annual deals that benefit refiners.

Mazumdar said that the majority of mines produce copper concentrate, for which 50 percent of the smelting capacity is in China. The end price is dictated by treatment and refining charges, which he said have gone low and nearly turned negative.

He went on to say that the other price to look at when analyzing copper markets is copper cathode premiums, which reflect cathode supply and demand.

“So there’s the cathode price. That’s stated in the London Metals Exchange, and Shanghai and the COMEX in the States. But if the market is tight in any of those regions, locally, you will see a cathode premium … over the price of the copper,” Mazumdar said. “People are willing to pay more to incentivize people that have copper inventory to actually put it into the market.”

According to Mazumdar, the current low treatment and refining charges and high cathode premiums are indicative of a very tight near-term market.

Electrification driving copper demand

Higher prices also reflect a recovery from manufacturing sectors as well as higher demand from industries tied to the global energy transition.

Electricity generation in general is a large driver of copper demand, and renewable energy options such as solar and wind consume even large amounts of copper. This is significant as the world continues to move away from fossil fuels, the need for both wind and solar will drive the need for materials to produce parts for turbines and photovoltaics, including copper.

In its Short-Term Energy Outlook, the US Energy Information Administration reported that US electricity generation increased 5 percent during the first six months of 2024 compared to H12023, and predicted that electricity in the second half of 2024 would be up 2 percent compared to last year.

The report also indicates that solar is currently the fastest-growing source of electricity generation. Solar generation was up significantly in the US year-over-year in H1, and the EIA expects it to grow 42 percent year-on-year during the second quarter.

This comes alongside increases in installed solar and wind, particularly in China, which saw record-setting installations of wind and solar projects as installed solar costs drop below that of any other energy source.

Renewable usage is also increasing with corporations. S&P Global Commodity Insights reports that corporate renewable capacity has increased by 15.8 gigawatts worth of contracts being signed through the first quarter, representing a 36 percent increase from the same time in 2023. Of those, solar led the way and made up roughly half of the deals signed.

The report indicated the mineral extraction sector saw strong renewable growth, including 2.5 gigawatts of deals signed by Rio Tinto (LSE:RIO,NYSE:RIO) as it works to improve its carbon footprint at its Australian operations.

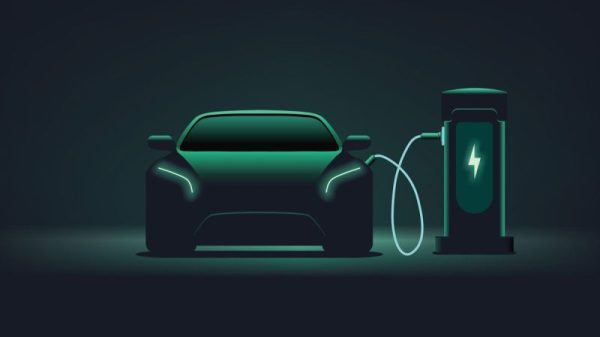

Significant copper demand has also been coming from electric vehicle (EV) producers who have been trying to meet growth in the automotive sector. Since 2023, there have been reports of a slowdown in EV sales, but many US carmakers have strong growth in 2024.

During the first half of the year, US EV sales saw an 11.3 percent increase over 2023 with 330,463 units sold. Globally, sales were even stronger, increasing 20 percent to 7 million units sold. China held its position as the strongest EV market, accounting for 4.1 million of those sales.

EVs can use as much as 60 kilograms of copper versus the 25 kilograms in traditional internal combustion powered cars and 29 kilograms in hybrids. Additionally, the electrical demands on the grid will require more power generation and thus even greater amounts of copper.

In a May 2024 report from the International Energy Forum, a body established to facilitate dialogue between energy-producing and energy-consuming countries, it suggested that current goals for 100 percent EV production by 2035 were unrealistic. Instead, it recommended the goal be moved to the manufacturing of hybrids instead.

It noted that the average copper production output of the top 10 mines is 472,000 metric tons per year, and in order to maintain current increases to demand 1.1 new mines will need to be added every year until 2050. When EVs and their demands from the electric grid are factored in, that rises to 1.7 new mines per year or 54 new mines by 2050.

What can copper investors expect in 2024?

In the short term, there is still copper supply in the market, but the situation could quickly change. The Chinese real estate market, which has traditionally been a major demand generator for copper, hasn’t recovered yet, and a shift there could send an already tight market over the edge.

Chinese officials have made attempts to revive the flagging sector, but the initiatives have had little effect and are threatening to drag its economy down further.

However, in China, softened copper demand from housing has largely been offset by increased demand from EVs and the country’s attempt to move away from fossil fuel to meet its energy needs.

As for incoming supply, Mazumdar noted that funding for projects tough as due to rising costs, and the copper price hasn’t been enough to incentivize it. Additionally, projects that have seen development won’t come online in time to fill gaps in production as they’ve also been held back.

He suggested producers are looking to avoid the kind of cost overruns experienced with Teck’s (TSX:TECK.A,TECK.B,NYSE:TECK) Quebrada Blanca 2 expansion, which ballooned from US$4.7 billion to US$8.8 billion.

Additionally, while mergers and acquisitions are taking place in the industry, they have largely been focused on producing assets.

“They don’t mind paying a premium for a project in production because it’s permitted, obviously, the tailings are organized and the capital has been spent, so there is no capital escalation risk,” Mazumdar said.

Mazumdar also suggested that permitting issues are a major factor to timelines, causing investors to rethink where their capital flows to. These long permitting times are resulting in companies turning to jurisdictions with more government support for critical metals, citing Barrick’s (TSX:ABX,NYSE:GOLD) projects in Pakistan.

“Why spend a premium on a project that might take 10 plus years to permit when you can spend as much or less on a project that you can get funded in an area that might take half the time to put into production,” he said.

With limited supply and little to be done to ease permitting times, copper demand is likely to keep the market bullish. This demand is likely good news for investors looking to find opportunities in the resource sector as copper is critical in the medium and long term to energy transition goals around the world.

Securities Disclosure: I, Dean Belder, hold no direct investment interest in any company mentioned in this article.